‘Thrown to the wolves.’ Investors rule Lexington’s housing market. Locals get what’s left.

READ MORE

Lexington’s housing market

A Herald-Leader analysis found that 235 investors controlled one in every 10 Lexington home sales since 2019.

Expand All

‘Thrown to the wolves.’ Investors rule Lexington’s housing market. Locals get what’s left.

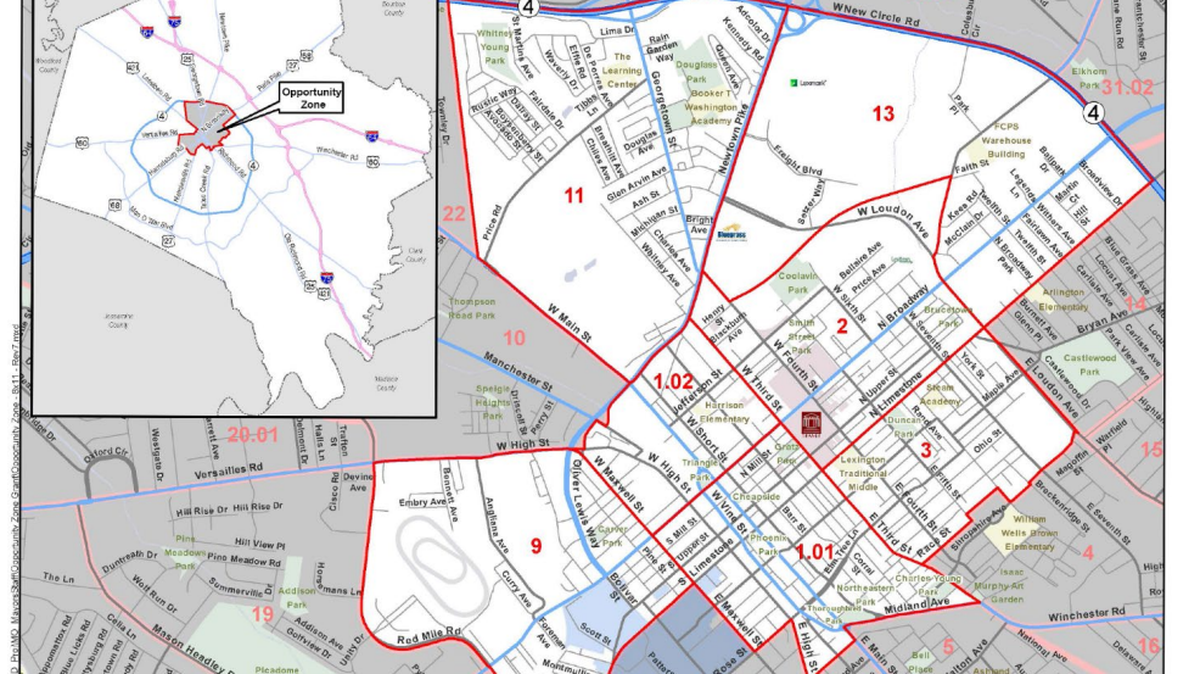

Some investors get big tax breaks for buying houses in low-income ‘opportunity zones’

Meet the top investors who have bought nearly 1,000 Lexington homes since 2019

Airbnbs are popular and profitable. Do they also drive up Lexington housing costs?

‘I’ve lost my home, I’ve lost a lot of my belongings, I’ve lost my friends.’

Nancy Cox’s introduction to Lexington’s real estate investors came in May when a letter arrived from her longtime landlord.

He revealed that he had just sold the boxy, brick Carr Building on the 1000 block of North Limestone Street, where Cox and her neighbors each lived for $550 a month.

The building’s new owner, who is one of the city’s biggest real estate investors, planned to renovate the place and charge higher rents that would better reflect the gentrifying neighborhood. Residents of the eight small apartments had 45 days to get out.

And nowhere else were $550 apartments available anymore.

“I asked, ‘What are we supposed to do? Where are we supposed to go?’” a tearful Cox, 61, recalled in a recent interview. “It was like being thrown to the wolves.”

Across town, Ashley Crossen ran headfirst into the investors last year when her family tried to buy an affordable home in southwest Lexington’s Stonewall neighborhood, an attractive 1960s suburb just outside New Circle Road.

Crossen and her husband always seemed a step behind the cash-loaded deal makers, who typically bid above asking price for the modest houses on tree-shaded streets. Investors snapped up properties and flipped them with cosmetic improvements (“four-inch Breccia Paradiso marble countertops!”) and jaw-dropping price hikes.

A house on Roxburg Drive sold for $300,000 on Feb. 14, 2020, and flipped six months later for $395,000. Another on Buckingham Lane sold for $200,000 on Jan. 14, 2021 and flipped 14 months later for $365,000. A third on Wellington Way sold for $254,000 on Aug. 13, 2021, and flipped for $380,000 in just three months.

“It was really irritating. They were buying these places sight unseen, over the phone,” Crossen said. “I was stalking the LBAR and Zillow apps, and when a house would go up, I would call right away to schedule an appointment. But it had already sold.”

Cox and Crossen aren’t the only ones feeling burned.

Over the last three-and-a-half years, a few hundred real estate investors had an over-sized impact on Lexington’s housing market, according to publicly available property data.

Their deals tightened supply and raised costs in a fast-growing city of 320,000 where lack of affordable housing already was a serious problem because of a slowdown in housing construction since the mid-2000s and an Urban Services District that places much of Fayette County off-limits to development in order to protect farmland.

The Herald-Leader studied 26,835 residential property purchases in Lexington from 2019 through this summer, using sales data from the Fayette County Property Valuation Administrator.

The majority of those transactions were simply people buying a home in which to live.

However, the newspaper identified 235 investors who bought five or more residential properties in this period, usually through limited liability corporations, which provide a number of tax and legal advantages for people who plan to make money off a house without ever living in it.

This pool of 235 investors accounted for one in every 10 residential property purchases in the city.

Data from the Fayette County PVA shows that, overall, 18 percent of residential property sales in Lexington in the years 2019, 2020 and 2021 went to LLCs rather than individuals. Of that group, the percentage of out-of-state LLCs rose from 5 percent in 2019 to 12 percent last year, accounting for several hundred home sales.

On just one random street — the three blocks of Preston Avenue in Lexington’s popular Kenwick neighborhood, southeast of downtown — 12 of 34 sales since 2019 went to corporations rather than individuals.

In most cases, the houses flipped within months with a hefty price increase. At least two Airbnbs are now advertised on Preston Avenue.

‘Build wealth and passive income’

Lexington mirrors a national trend, with investors showering homeowners with pleas to buy their houses, in any condition, through roadside signs, direct mail, phone calls and texts, and online and broadcast advertising. They also bought hundreds of houses at Fayette County foreclosure sales when homeowners fell behind on their debts.

Studies have documented a rise in activity by housing investors across the country over the last few years, with a notable impact on housing prices.

Deals by investors boosted national housing costs — sale prices and rents — by more than 20 percent on average, according to an analysis released in January by Mark Zandi, chief economist for Moody’s Analytics.

“This is not a healthy market,” Zandi wrote. “It feels like it is getting stretched very thin.”

There are all sorts of investors in Lexington.

Some investors rebuild aged, dilapidated houses that were abandoned long ago and give them productive new lives, while others gobble up cheap starter homes that would have been ideal for young families.

Some accumulate vast portfolios of rental housing for long-term tenants or short-term use, such as Airbnb vacation getaways. Some quickly flip houses, not wanting to hold them for any longer than they have to.

There are local entrepreneurs who got into real estate while they were still youths attending college, like Jeff Moore and Scott McIntosh; large out-of-state corporations, like Amherst Holdings LLC of Austin, Texas, and BRG Realty Group LLC of Cincinnati; and successful doctors with spare cash to invest, like Maria Cristina Atienza of Corbin and Adil Mohammed Mohiuddin of Louisville.

There are wealthy individuals who see a chance to get even richer, such as former Harvard rowing crew mates and Google tech executives Tom Fallows and Jonathan Kibera of San Francisco, who have bought eight small Lexington homes through their corporation, SFR3 LLC. (“SFR” is industry lingo for “single family residence.”) In some cases, they bought homes that were owned by the same people for decades.

Another such investor is Grant Gustavson of Las Vegas, whose grandfather, billionaire B. Wayne Hughes, was reportedly Kentucky’s richest man when he died last year.

In 2018, the year after he graduated from the University of Southern California, Gustavson earned $135,000 as acquisitions officer for one of his grandfather’s companies, American Homes 4 Rent, according to public records.

Gustavson is now raising money for his own rental company. My Income Property LLC last year bought 10 family homes around Lexington to lease to tenants. “Build wealth and passive income through real estate,” the company urges potential investors, adding that rents at its houses — between $1,500 and $2,000 — should grow by 6 percent annually.

This is a profitable time to buy Lexington housing ahead of the locals who need a place to live, the company told potential investors in a filing with the U.S. Securities and Exchange Commission.

“The housing market is significantly under-supplied,” My Income Property said.

“In addition to this supply vs. demand imbalance, the rapid increase in home prices and heavily indebted balance sheets for the median renter further supports renter demand,” it said. “Due to these reasons, above-inflation market rent growth and occupancy near or at all-time highs are projected over the next few years.”

Quick buck or investment?

Real estate investors have made waves in Lexington for a while, said Charlie Lanter, the city’s commissioner of housing advocacy and community development.

“It’s not really new, but yes, the last five years or so, we are seeing more of it,” Lanter said.

“The usual pattern has been, a corporation would come in and buy an apartment complex, slap a fresh coat of paint on the place, maybe upgrade the landscaping. Then it jacks up the rent by 25 percent,” Lanter said.

“That displaces a lot of the tenants, who obviously can’t afford to live there anymore,” he said. “And as they are forced to look for housing elsewhere, some of them end up bumping other people from their places, and then the more the problem spreads, the crummier the quality of the available housing that remains.”

Urban County Councilman James Brown says he sees the entire picture. Brown is a real estate agent who also represents the 1st District, including low-income downtown neighborhoods being transformed by investors into upscale housing for young professionals who want to live within walking distance of dining and live entertainment.

“To me, it’s all about the intent,” Brown said.

“Are you looking to create more safe, affordable housing?” Brown asked. “If that’s your intent, then by all means, have at it. But if your intent is just to flip some houses or displace people to make a quick buck, then that’s not what we need. It’s not what our neighbors want.”

“I think there are some people who are doing that, but I also talk to those who are in it for the long run, investing in our community,” the councilman said.

Some need not apply

Cox came to Lexington from her hometown of Nicholasville in the 1970s when she was 21. She has held different low-wage jobs — household maid, laundry worker, deli waitress — and she always lived on North Limestone. Her friends lived in that neighborhood, too. Her church, Zion Baptist, was just down the block.

She moved into one of the Carr Building’s upstairs apartments 13 years ago. The residents tended to be older, often with disabilities, she said. Having found a cheap place to roost, they stayed put and looked out for each other.

“There were people who had been up there for 20 years,” Cox said. “We were like a family up there. Most of us didn’t have anybody else.”

So Cox watched nervously as the North Limestone neighborhood — fashionably dubbed “NoLi” in modern real estate listings — began to gentrify, pushing aside the poorer people who were there first.

Local and national LLCs bought a dozen residential properties within five blocks of the Carr Building in either direction along North Limestone. Investors rehabilitated old buildings throughout the area, opening cool bars and restaurants and leasing modernized apartments to young people for $1,400 a month. At the Greyline Station, a 65,000-square-foot dining and retail complex that opened nearby, a vegan Italian sausage sells for $14.99. (Editor’s Note: The Herald-Leader currently leases office space in Greyline Station.)

Many investors not only raised the rents around Cox’s neighborhood, they refuse to accept federal Section 8 housing vouchers for low-income tenants. For further screening, they instruct applicants to provide good credit scores, proof that their income is at least three times the rent and favorable background references.

Other cities require landlords to accept Section 8 vouchers for the poor, including Louisville, but Lexington does not. This excludes a lot of families. There are nearly 3,500 Section 8 participants in Lexington, with hundreds more on the waiting list, according to the Lexington Housing Authority.

In some of Lexington’s gentrifying neighborhoods, rents are climbing so high that the cost of housing exceeds the spending limits of Section 8 even if the landlords were open to it, said Aldean Pleasant, who manages the voucher program for the housing authority.

“The area along Georgetown Street is a prime example of where rent has increased so fast,” Pleasant said. “Over here in the Winburn neighborhood, the rent on a single-family home has increased by three digits. That really limits our participants’ ability to find better housing in a better neighborhood.”

Landing far from home

Cox kept asking her landlord if he planned to sell the Carr Building, she said, and he kept promising her that he wouldn’t — right up until the day that he did.

The residents, some of whom had leases, were relocated to make way for the new owner’s renovations. Tipped off to their misfortune, the city of Lexington’s affordable housing office helped them find new apartments and provided them with public subsidies to cover their security deposits and higher rents for several months.

“Our first thought was ‘Oh no!’ Because there’s not another place in Lexington where you can find an apartment for $550 a month,” said Lanter, the commissioner for housing advocacy.

Cox landed in a tiny studio apartment two miles away, just off Jefferson Street, for $740 a month.

She’s too far from her old neighborhood to walk back and see her friends. She doesn’t own a car. Her monthly income from Social Security and disability is $840. After she pays her cell phone and health insurance bills, she doesn’t know how she’ll balance her checkbook without the city’s subsidies, which expire soon.

The experience has left her embittered about the changes real estate investors are bringing to the city.

“I understand they’ve got a right to make money. But this is how you get homeless people,” Cox said. “You take away the places they have to live and you don’t leave them anyplace else they can afford.”

‘Nothing personal, it’s business’

Shane Eckman is the man who bought the Carr Building last spring.

Eckman, 48, is one of Lexington’s biggest landlords. He owns about 160 residential properties through different LLCs. He went on a buying spree the last few years, picking up the portfolios of landlords as they cashed out and spotting individual deals he liked around North Limestone and Loudon Avenue.

His rents in this area can range from about $650 to $1,250, depending on the size of a unit, Eckman said. He’s had conversations with Vice Mayor Steve Kay about the need for more family housing, so he tries to offer places with multiple bedrooms at reasonable prices, he said.

“This is a great neighborhood,” Eckman said one sunny morning, standing outside several of his rental properties on East Loudon. “There are a lot of amenities here. The park, the pool, the Friday night market. You can walk places.”

With its cheap older homes near downtown, the area around Loudon Avenue today is a lot like the Kenwick neighborhood was 25 years ago, he said.

“Kenwick is not affordable anymore for a young person,” Eckman said. “But young people or young families, they could come in here and find an affordable place to buy.”

He paused.

“That’s rapidly changing,” he added.

Eckman, who spent part of his own youth in a Nicholasville trailer park, said he feels badly about what happened to Cox and her neighbors in the Carr Building. The previous owner assured him that nobody had a lease, which did not prove to be correct, he said.

The place was in terrible shape, he added. He’s spending about $200,000 to replace the flooring, the wiring, the plumbing and the appliances and to bring everything up to code.

“You opened a stove over there and roaches came out,” Eckman said.

When the work is finished, he said, the Carr Building apartments might rent for up to $700 a month. Any of the previous tenants are welcome to return, he said.

One of Cox’s former neighbors, Pete Humphries, was the last to leave the Carr Building, along with his girlfriend. They stayed through most of the summer while construction workers loudly ripped the place apart and rebuilt it outside their apartment door.

Humphries said he doesn’t hold a grudge against Eckman, who is moving the couple into one of his many rental houses for the discounted price of $850 a month. The place usually leases for $1,250, Humphries said, but Eckman agreed to be charitable, given the circumstances.

While his previous $550 rent can’t be beat, it’s hard to get too nostalgic about the Carr Building, said Humphries, who lived there for less than a year.

“That place should have been condemned,” Humphries said. Regarding Eckman, he said, “It’s nothing personal, it’s business. I understand. He wants to fix this place up.”

Doctors buying houses

Of the 235 real estate investors who bought five or more places since 2019, at least 18 are doctors by trade.

Dr. Maria Christina Atienza and Dr. Arden Marciano Acob run a medical practice together in Corbin. They’re also partners in Crisden Properties LLC, which just bought its ninth Lexington residential property in the last three years. They’ve spent about $1.2 million so far, according to public sales data.

They began with one townhouse that Atienza wanted so her young daughter would have a place to live when she grew older and attended high school in Lexington. But the deals were so good — tenants are practically begging to move in and pay rent, Atienza said — that the doctors kept picking up more places.

The only obstacle is the intense competition for reasonably priced family homes, which even investors can face, Atienza said. One bidding war led to 30 offers for a place. Another seller, with a house near the UK campus, said he had 13 offers and wouldn’t hear any more after the noon deadline. But Atienza really wanted that one.

“We bid on it without even getting to look inside,” she recalled, laughing. “It was, like, 11 a.m. Our Realtor had to put everything together in 20 minutes. He said that was the fastest he ever put an offer together. And you know what? We got the house!”

Another physician, Dr. Adil Mohammed Mohiuddin, purchased at least 45 residential properties in Lexington over the past three years, operating through three corporations, A Zahed Properties LLC, Adil Properties LLC and Zahed Property Management LLC. He is now one of the city’s larger landlords.

Born and educated in Hyderabad, India, Mohiuddin works at Jane Todd Crawford Hospital in Greensburg. He did not respond to requests for comment for this story.

Ilka Tait, 49, lives with her son in one of Mohiuddin’s properties, a house on the 600 block of Anniston Drive. The Lexington Division of Code Enforcement repeatedly cited the house for violations this year, including deficiencies with its roof, walls, front door and bathroom. And it ordered Mohiuddin to properly install smoke detectors.

Tait said she realized after she moved in that the $1,250-a-month house is “a hot mess,” but Mohiuddin refused to make repairs until she called city inspectors. Only then, she said, did he send a repair crew that dragged its feet — hence, the follow-up citations from code enforcement this summer and subsequent fines of nearly $300.

Among the house’s deficiencies, Tait said: a gap under the front door let mice and other pests freely enter; the air conditioning failed; the roof leaked; and mold and mildew spread through the rooms, aggravating her son’s health problems.

“I was standing there one day by the front window when a big rainstorm started,” said Tait, who works in the neurology department at a Lexington hospital. “Suddenly, I felt water dripping on my head. I was like, ‘What?’ I looked up and there was a big hole in the roof above me.”

Tait submits her rent to a third-party online portal. But one day, she did the necessary sleuthing to figure out who owns her home and where he’s employed. She phoned Mohiuddin to complain about her living conditions.

The conversation did not go well, she said.

“He was offended,” she said. “He said, ‘You called me at work! Don’t you do that again.’”

‘Rent growth should remain high’

Over the summer, Danielle Thompson moved into a $1,595-a-month, three-bedroom rental house on Walcot Way in a four-year-old subdivision off Georgetown Road, near the Scott County line.

Actually, the first home she tried to move into in that subdivision had a squatter illegally living in it, to her great surprise, Thompson said. The management company offered her the keys to a second house around the corner. That place was blessedly free of other occupants, but it was no great prize, she said.

“They said it was ‘Move-in ready.’ It was not,” said Thompson, 26, a financial stability coordinator at a Lexington nonprofit. “I had to deep-clean everything down to the floors and the window blinds. And there wasn’t a refrigerator in the kitchen, which is obviously something that you’re going to need.”

Thompson’s house — and 70 more around it — is owned by Amherst Holdings LLC of Austin, Texas, which last December bought the subdivision through subsidiaries including BAF 1 LLC and BAF Assets 4 LLC. Investor-backed Amherst has acquired more than 50,000 homes nationally that are worth approximately $8.6 billion.

In a prepared statement to the Herald-Leader, Amherst said: “We invest the capital needed to provide durable flooring, roofs and siding, stainless steel appliances and access to professionally managed services. We also employ local contractors in the Lexington metro area to support the local economy while providing our residents with access to quality and timely maintenance.”

Like other large institutional investors, Amherst predicts a bright future in charging people for the roofs over their heads. Amherst’s annual 20-city single-family home “rent-growth index” stayed at an impressive 10.8 percent for the months of May and June.

“In response to ownership becoming increasingly more expensive and less attainable, Amherst believes rent growth should remain high in the short term as households turn to homes for lease as a more affordable way to access single-family homes,” the company told potential investors in August.

Thompson said she reluctantly agrees with Amherst’s rosy investor outlook. You can search a long time for decent, affordable housing in Lexington, and after a while, you learn not to get too picky, she said.

“It is absolutely a landlord’s market and a seller’s market,” she said.

Turmoil could be coming

But nobody knows if the next few years will be as golden for real estate investors, or if some — especially smaller, newer investors — will run into financial trouble, causing more turmoil in Lexington’s housing market.

“I think we’re going to see the bubble tip back,” said longtime Central Kentucky investor Jonah Mitchell, who teaches a real estate class at the University of Kentucky Gatton School for Business.

“They’ve gobbled up all the low-hanging fruit already,” Mitchell said. “I think the curve will start going the other way.”

The economic landscape is changing.

Interest rates plunged in 2018, making it far cheaper to borrow money — and an investor scooping up dozens of residential properties might be carrying millions of dollars in debt, assuming that he can make a profit either in the short run, from flipping and selling properties, or in the long run, from rents and, eventually, cashing out.

But for investors, long-term loans tend to be a 5/1 adjustable-rate mortgage, not the fixed-rate 30-year note that most homeowners get. That’s a technical way of saying that after five years, the banks can raise their interest rate, and they can keep raising it for each of the years remaining on their loan.

When interest rates are soaring, as they presently are, investors with a portfolio full of adjustable-rate mortgages anxiously wonder how much more their loans soon will cost them.

A lot of new people jumped into real estate in the last few years and made their business plans based on interest rates in the neighborhood of 2 to 4 percent, said Jeff Moore, who is one of the city’s top residential investors. Their plans might collapse if they’re required to start paying 10 percent to 12 percent, Moore said.

“When the tide goes out, a lot of people are going to get hurt,” Moore said. “Unfortunately, with real estate, it won’t just be the landlords who get hurt, it’s also going to be the tenants and the neighbors.”

Mitchell said he agrees with this warning.

“I’ve got a friend who says we borrowed with good money and we’re going to be paying it back with inflated money,” Mitchell said.

“You should be OK as long as you’re not over-extended, as long as you have enough equity in your properties,” he said. “But if you don’t, then you’re going to have a problem.”

This story was originally published October 20, 2022 at 10:35 AM.